A consumer complaint is easier to file when you know where it belongs.

The problem is that many agencies sound similar.

A scam may feel like an FTC issue. A credit card problem may belong with the CFPB. A dangerous product may need CPSC. A phone or internet billing problem may fit the FCC. A local landlord, contractor, car dealer, or store dispute may need your state attorney general or state consumer protection office.

If you send the complaint to the wrong place, it may not disappear, but it may not move as quickly as you hoped.

A good complaint starts with routing.

Ask:

What happened?

Who is the company?

What product or service is involved?

What result do I want?

Which agency handles this type of problem?

This guide maps common consumer problems to the right US complaint channel.

First, try the company when it is safe

Before filing with an agency, try to resolve the issue directly with the company if the problem is a normal service, billing, refund, delivery, or warranty issue.

Contact the company and save:

Date of contact

Person or department contacted

Chat transcript

Email thread

Case number

Receipts

Order number

Account number, partly masked

Photos

Screenshots

Warranty terms

Return policy

Payment proof

What you asked for

What the company said

But do not keep arguing forever.

If the company ignores you, refuses to explain, misleads you, keeps billing you, delays refund, or the issue involves fraud, danger, or repeated harm, move to the right complaint channel.

For scams, unsafe products, identity theft, or urgent financial harm, do not wait too long.

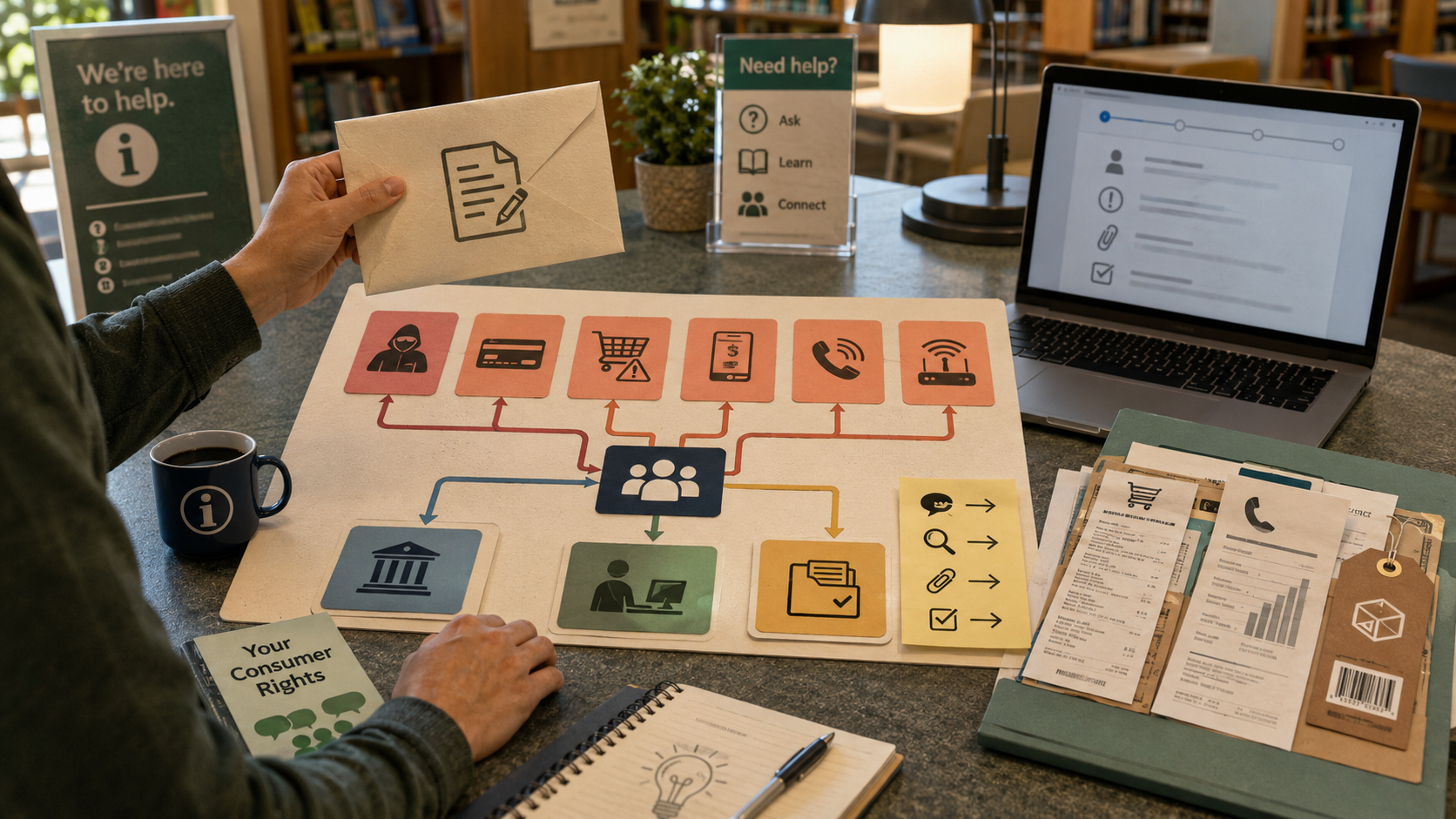

The quick routing map

Use this as the first pass.

FTC

Use for scams, fraud, identity theft, fake business practices, misleading advertising, unwanted business behavior, fake prizes, impostor scams, online shopping scams, subscription traps, and general bad business practices.

CFPB

Use for consumer financial products and services: credit cards, bank accounts, credit reports, debt collection, mortgages, student loans, personal loans, auto loans, money transfers, and payment issues.

CPSC

Use for unsafe consumer products: toys, appliances, furniture, batteries, electronics, child products, household products, and product injuries or hazards.

FCC

Use for phone, internet, TV, radio, accessibility, unwanted calls and texts, robocalls, number spoofing, phone billing, broadband service, and communications issues.

State attorney general or state consumer office

Use for local businesses, contractors, landlords where covered by state rules, car dealers, local stores, state-specific consumer laws, price gouging, home repair, local scams, and complaints that need state-level enforcement or mediation.

Some problems may fit more than one place.

That is normal.

Start with the agency closest to the product or service involved.

When to use the FTC

The Federal Trade Commission is a good place for fraud, scams, deceptive business practices, and many unfair or misleading consumer problems.

Think FTC when the issue sounds like:

Scam

Fraud

Fake company

Fake prize

Fake job

Impostor

Fake government message

Online shopping scam

Subscription trap

Misleading advertising

Identity theft

Fake tech support

Fake debt relief

Fake investment pitch

Romance scam

Gift card scam

Crypto scam

Business refuses to honor obvious promises

Seller disappears after payment

Company uses deceptive marketing

Examples:

You paid for an online product that never arrived and the seller disappeared.

A fake delivery message asked for a fee.

A company promised a free trial but kept billing.

Someone pretending to be a government agency demanded gift cards.

A fake job asked you to deposit a check and send money back.

A website used misleading claims to get payment.

The FTC may not solve every individual complaint like a customer service desk. But reports help law enforcement spot patterns and take action.

Use FTC when the problem is about deception, fraud, or broad bad business conduct.

When to use the CFPB

The Consumer Financial Protection Bureau is the right fit for many money-account and financial-service complaints.

Think CFPB when the issue involves:

Checking account

Savings account

Credit card

Credit report

Credit score or reporting error

Debt collection

Mortgage

Student loan

Auto loan

Personal loan

Payday loan

Buy now, pay later, where covered

Money transfer

Payment app

Prepaid card

Credit denial

Bank fees

Account closure

Unauthorized transaction

Loan servicing

Debt collector behavior

Examples:

Your credit report shows an account that is not yours.

A bank charged fees you believe were not disclosed.

A credit card company will not correct a payment issue.

A debt collector keeps contacting the wrong person.

Your mortgage servicer is not applying payments correctly.

A student loan servicer gives conflicting information.

A money transfer problem is not resolved.

The CFPB complaint process usually sends your complaint to the company for response.

Use CFPB when the problem is with a financial company or financial account.

When to use the CPSC

The Consumer Product Safety Commission handles many safety issues involving consumer products.

Think CPSC when the issue involves:

Unsafe toy

Appliance fire risk

Battery overheating

Furniture tip-over risk

Child product hazard

Product injury

Defective household item

Power tool hazard

Electronics overheating

Product choking hazard

Product laceration hazard

Product burn hazard

Product recall concern

Unsafe crib, stroller, high chair, or carrier

Dangerous home equipment

Examples:

A space heater overheats and melts plastic.

A toy breaks into small sharp pieces.

A dresser tips over easily.

A battery pack swells or smokes.

A stroller part fails.

A kitchen appliance sparks during normal use.

A recalled product is still being sold.

Use CPSC or SaferProducts.gov when the central issue is product safety.

This is different from a normal refund complaint.

If the product is unsafe, report the hazard even if you also ask the retailer for a refund.

When to use the FCC

The Federal Communications Commission handles many communications-related complaints.

Think FCC when the issue involves:

Phone service

Mobile carrier

Internet service

Cable TV

Satellite TV

Radio

Robocalls

Unwanted texts

Caller ID spoofing

Phone billing

Broadband speed or service

Number porting

Accessibility for communications services

Emergency communication access

Slamming or cramming in telecom billing

Do Not Call-related communications issues, where applicable

Examples:

Your phone company bills you for services you did not authorize.

Your internet provider does not fix a service problem.

You get repeated robocalls or spoofed calls.

A carrier refuses to release or port your number.

A cable or satellite TV billing issue is unresolved.

You have an accessibility complaint about a communications service.

Use FCC when the core problem is communication service, not a general shopping dispute.

If the issue is a scam text asking for money, the FTC may also fit. If the issue is unwanted texts or robocalls, the FCC can be relevant too.

When to use your State Attorney General or state consumer office

State attorneys general and state consumer protection offices are useful for local and state-specific consumer issues.

Think state AG or state consumer office when the issue involves:

Local business

Contractor

Home repair

Landlord or tenant issue, depending on state resources

Car dealer

Auto repair shop

Local store

State price gouging rules

Local scam

State licensing issue

Warranty issue with a local company

Moving company problem

Funeral services complaint

State-regulated professional

Door-to-door sales

Home improvement fraud

Business operating in your state

Examples:

A contractor took a deposit and disappeared.

A used car dealer misrepresented a vehicle.

A local business refuses to honor a written agreement.

A landlord or property manager dispute needs state-specific guidance.

A store is accused of price gouging during an emergency.

A moving company adds unexpected charges.

A home repair company pressures an older adult into a bad contract.

State offices vary. Some investigate patterns. Some mediate complaints. Some refer you to another agency. Some handle specific industries through separate state boards.

Use state resources when local law, local licensing, or state consumer rules matter.

Problems that may need more than one complaint

Some situations cross agency lines.

That does not mean you did anything wrong.

Example:

A fake online seller takes payment and ships a dangerous counterfeit charger.

Possible channels:

FTC for the fraud or deceptive seller

CPSC for the unsafe product

Payment provider or credit card issuer for dispute

Marketplace support for seller report

State AG if the seller is local or the pattern affects your state

Another example:

A debt collector sends threatening robocalls.

Possible channels:

CFPB for debt collection

FCC for unwanted calls

State AG for local enforcement or state debt collection rules

FTC if the collector appears fake or deceptive

Choose the strongest primary channel first.

Then report the other parts where they fit.

Do not send every complaint everywhere automatically

Filing everywhere can feel productive, but it can also create confusion.

Before sending multiple complaints, ask:

What is the main problem?

Which agency clearly handles this category?

Is there a safety issue?

Is there a financial account issue?

Is there a communication service issue?

Is there fraud?

Is there a state or local business issue?

What result do I want?

Start with the best match.

Add another complaint only if there is a separate issue that fits another agency.

What to include in any complaint

No matter which agency you choose, prepare the same basic packet.

Include:

Your name and contact information

Company name

Company address or website, if known

Account or order number, partly masked where appropriate

Dates

Amounts

Product or service involved

What happened

What you already tried

What the company said

What result you want

Receipts

Screenshots

Photos

Contracts

Warranty terms

Bills or statements

Case numbers

Delivery proof

Payment proof

Names of representatives, if available

Keep the complaint clear.

Do not write 10 pages if one page will explain it.

A strong complaint tells the story in order.

Use a simple complaint structure

Use this structure:

1. What happened

Say the problem clearly.

2. When it happened

List dates.

3. What you paid or lost

Include amount.

4. What you asked the company to do

Refund, repair, correction, cancellation, investigation, explanation, or account fix.

5. What proof you have

Receipts, photos, statements, screenshots, emails, letters.

6. What result you want now

Be specific.

Example:

“I want the $146.22 duplicate charge refunded and written confirmation that the subscription is cancelled.”

Specific requests are easier to respond to than general anger.

Match the request to the agency

Do not ask the wrong agency for something it cannot directly do.

For example:

FTC reports may help enforcement, but may not get you an individual refund immediately.

CFPB can route many financial complaints to companies for response.

CPSC focuses on product hazards and safety.

FCC handles communications-related complaints and inquiries.

State AG offices may mediate or investigate depending on state rules and resources.

This does not make complaints useless.

It means you should understand the role.

For personal refunds, also use company escalation, payment dispute rights, warranty claims, chargeback process, small claims court, or local legal help where appropriate.

Before filing: choose the right channel

Use this decision path.

Is it a scam, fraud, fake business, or deceptive marketing?

Start with FTC.

Is it a bank, credit card, loan, credit report, debt collection, mortgage, or money transfer issue?

Start with CFPB.

Is the product physically unsafe or causing injury risk?

Start with CPSC or SaferProducts.gov.

Is it phone, internet, TV, radio, robocalls, unwanted texts, or telecom billing?

Start with FCC.

Is it a local business, contractor, car dealer, landlord, home repair, or state-law issue?

Start with your state AG or state consumer office.

Is it a vehicle safety recall?

Use NHTSA, not CPSC.

Is it food, medicine, medical device, cosmetics, or supplement safety?

Use FDA complaint or recall channels, not CPSC.

Is it workplace discrimination or wage theft?

That may involve other labor or civil rights agencies, not these consumer complaint channels.

This article focuses on consumer complaints, not every legal problem.

Common complaint examples

Fake online store

Best fit: FTC

Also consider: payment provider, marketplace, state AG if local

Credit report error

Best fit: CFPB

Also contact: credit bureau and company furnishing the information

Dangerous toy

Best fit: CPSC

Also contact: retailer or manufacturer for recall or refund

Robocalls and spoofed calls

Best fit: FCC

Also consider: FTC for scam patterns

Bank account fee dispute

Best fit: CFPB

Also contact: bank escalation first

Contractor took deposit and did not return

Best fit: state AG or state consumer office

Also consider: local licensing board, small claims court, police if fraud is involved

Subscription billed after cancellation

Best fit: FTC if deceptive or recurring billing issue

Also consider: card dispute and state AG

Internet provider billing problem

Best fit: FCC

Also contact: provider escalation

Product never arrived

Best fit: FTC if seller is deceptive or disappears

Also consider: credit card dispute, marketplace support, state AG

Unsafe appliance overheats

Best fit: CPSC

Also contact: manufacturer, retailer, and stop using until checked

Keep your own complaint log

Create a complaint log before filing.

Use:

Date filed

Agency

Company

Complaint number

Documents attached

Expected response

Company response

Next action

Deadline

Final result

This matters because complaints can take time.

A log prevents you from losing confirmation numbers, repeating the story, or missing deadlines.

Be careful with sensitive information

Complaints may need details, but do not overshare.

Avoid uploading:

Full Social Security number unless required and secure

Full bank account number unless necessary

Full card number

Passwords

One-time codes

Unredacted medical information unless relevant and safe

Personal details unrelated to the complaint

Use secure official portals.

Do not send sensitive documents through random links or email addresses you have not verified.

If you need to include account numbers, follow the agency’s instructions and redact where appropriate.

Do not confuse complaint filing with emergency help

Complaint agencies are not emergency services.

If there is immediate danger:

Call emergency services.

Stop using unsafe products.

Contact your bank immediately for active fraud.

Freeze or close affected accounts if needed.

Seek medical help for injury or poisoning.

Contact local authorities for threats or theft.

Use official recall instructions for serious hazards.

A complaint can come after immediate safety steps.

A realistic example

A reader buys a portable charger from an online seller.

The charger overheats, melts near the charging port, and the seller refuses a refund.

This is not only a refund issue.

The reader separates the problem:

Unsafe product: report to CPSC or SaferProducts.gov.

Online seller conduct: report to FTC if deceptive or unsafe selling pattern.

Refund: contact marketplace, seller, and payment provider.

Evidence: photos, order confirmation, seller messages, product label, and payment proof.

One complaint would not cover everything.

The safety issue goes to the safety agency.

The seller behavior goes to the fraud or business-practice channel.

The refund request goes through the seller, marketplace, or payment dispute path.

That is complaint routing.

The complaint routing checklist

Before filing, ask:

Is this mainly fraud or deceptive business conduct?

Is this mainly a financial account, loan, credit, or debt issue?

Is this mainly an unsafe consumer product?

Is this mainly phone, internet, TV, robocall, or communications service?

Is this mainly a local business or state-law problem?

Did I contact the company first, if safe and reasonable?

What result do I want?

What proof do I have?

Do I need more than one complaint because there are separate issues?

Have I saved confirmation numbers?

Then choose the channel.

Final thought

A complaint is more effective when it goes to the right place.

Use the FTC for scams, fraud, and deceptive business practices. Use the CFPB for financial products and services. Use CPSC for unsafe consumer products. Use the FCC for phone, internet, TV, robocalls, and communications issues. Use your state attorney general or state consumer office for local businesses and state-specific consumer problems.

You do not need to memorize every agency.

You only need to match the problem to the channel before you file.

That one step can save time, reduce frustration, and make your complaint easier to understand.

Reader Discussion

Comments

Comments are reviewed before appearing publicly.Reader comments